- RESEARCH BULLETIN NO. 69

- 15 April 2020

The growth of non-bank finance and new monetary policy tools

How does the presence of “shadow banks” – non-bank, unregulated financial intermediaries – affect the ability of central banks to tackle a liquidity crisis? To address this question, we develop an asset pricing model with both bank and non-bank financial institutions. A crucial part of the model is that banks intermediate liquidity between the central bank and non-banks, but this intermediation stops during a financial crisis. Non-banks are then left without a lender-of-last-resort, and central bank liquidity operations with banks are not sufficient to mitigate the crisis. In our stylized model, opening liquidity facilities to non-banks and purchasing illiquid assets are then essential measures to tackle a liquidity crisis.

Monetary policy and non-banks

Since the 1980s, in most advanced economies, the importance of non-bank financial institutions – such as investment funds and securities broker-dealers – has been steadily growing. This pattern holds in particular for the US financial system, with non-bank institutions holding more than double the financial assets of traditional banks. In Europe as well, non-banks have become an increasingly important source of financing for the real economy over the past decade (ESRB, 2019). This development brings many benefits in terms of diversification, but could also pose financial stability challenges. In particular, non-banks’ lack of access to central banks’ refinancing operations might create new obstacles in the transmission mechanism of monetary policy and for the role of lender-of-last-resort.

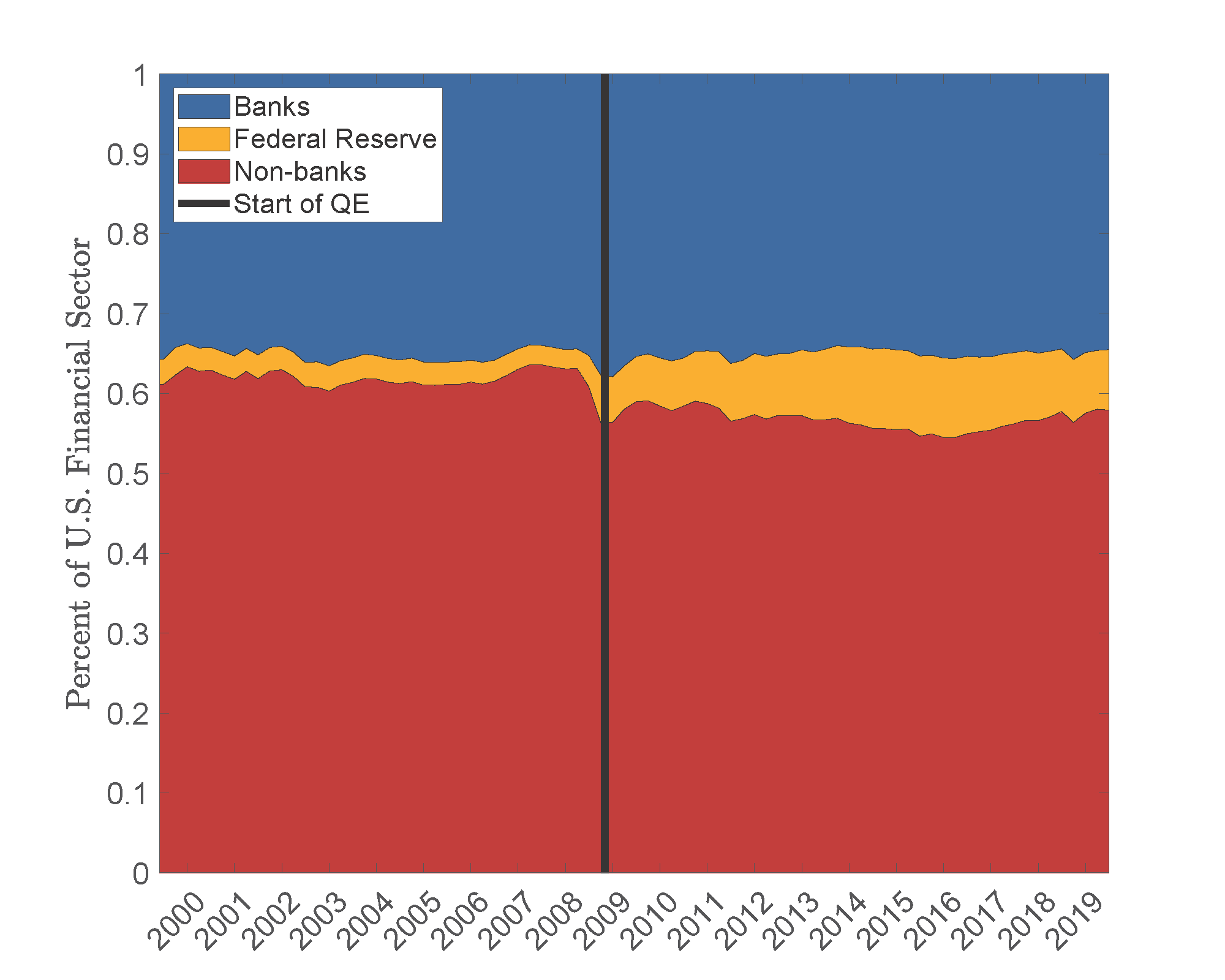

In fact, the existence of a large financial sector without direct access to the central bank is often considered a leading explanation for the severity of the 2008-09 crisis and the consequent expansion of monetary policy tools (Bernanke, 2009; Mehrling, 2011). In the United States, the Federal Reserve (the “Fed”) created various new lending facilities through which subsets of US non-banks could borrow against collateral when needed. As these new facilities still proved insufficient to satisfactorily stem the crisis, the Fed eventually resorted to the purchase of over USD 3 trillion of private securities to keep asset prices from dropping further and prevent contagion to the real economy. These securities were primarily sold to the Fed by non-banks, suggesting that the funding pressures were indeed mainly located in the non-bank sector. Meanwhile, traditional banks kept their share of asset holdings close to pre-crisis levels, as shown in Chart 1.

Chart 1

Evolution of the proportion of assets held by banks, non-banks and the Fed

Notes: The figure represents the evolution of the share of assets held respectively by banks (depository institutions), non-banks (money market funds, mutual funds, securities broker-dealer and government-sponsored enterprises) and the Federal Reserve System in the United States. Source: US Flow of Funds.

A new model of liquidity risk and non-banks

This narrative of the crisis and its monetary policy responses is prominent among economic commentators and central bankers. Yet it has not been fully incorporated into economic theory and the nature of the mechanisms at play remains largely unexplored. To fill this gap and contribute to the policy debate, in a recent working paper (d’Avernas, Vandeweyer and Darracq Pariès, 2019) we propose to amend the canonical “intermediary asset pricing model” from Zhiguo He and Arvind Krishnamurthy (2013) – which takes into account the special role of banks in determining the price of financial assets – to incorporate a non-bank sector and liquidity risk.

In the model, every financial institution is in the business of performing “liquidity transformation” by holding assets that are less liquid than its liabilities. For instance, a bank may do so by financing a long-term corporate loan with demand deposits from households. This liquidity mismatch between assets and liabilities generates liquidity risk for these institutions: faced with the pressure of a large outflow of funds, intermediaries may be forced to “fire-sell” some illiquid assets at a discount and bear a net loss.

In normal times, banks and non-banks efficiently minimise this liquidity risk by maintaining access to short-term money markets. After a negative funding shock, financial institutions of any type can borrow from money markets by pledging assets as collateral, instead of selling illiquid securities at a loss. However, when the value of the assets used as collateral becomes too volatile, these cannot be pledged anymore and liquidity risk shoots up. This higher liquidity risk leads in turn to a fall in asset prices, because financial intermediaries require a larger liquidity premium for holding risky financial assets. In this case, the central bank may intervene and reduce liquidity risk by providing central bank reserves – i.e. money for banks – to banks. As long as money markets operate efficiently, banks intermediate this liquidity received from the central bank to non-banks, which provides a relief to both funding and capital markets.

The distinguishing feature of our work is that we explicitly model non-banks, which do not have direct access to central bank interventions. Taking this institutional feature into account, we analyse the effect of monetary policy on asset prices. We consider three types of policies used in 2008-09: (i) increasing the supply of central bank money to banks; (ii) accepting a wider range of assets as collateral for the emergency lending facility; and (iii) directly purchasing illiquid assets.

What do non-banks change?

In an economy composed mostly of traditional banks, we find that the downward pressure on asset prices generated by liquidity stress can be efficiently mitigated by the first two traditional policy tools – increasing the money supply to banks and accepting broader collateral. By holding central bank money, banks build up a liquid buffer. They can then use this buffer to settle any debt after an unforeseen outflow of funds; it is an ex ante protection against liquidity risk, so that increasing the amount of cash reserves available to banks lowers liquidity risk and boosts asset prices. In addition, by accepting a wider range of assets as collateral or requiring a lower haircut than in private money markets at the emergency lending facility, the central bank increases the effective supply of loans for a given amount of collateral. This also reduces liquidity risk in banks.

We then perform a similar analysis in an economy in which there is a sizeable non-bank sector – as in the United States, both in 2008 and today. The main finding of our paper is that, in this case, traditional monetary policy tools are not sufficient. The intermediation of liquidity from traditional banks to non-banks relies on well-functioning money markets. As, in a crisis, virtually all money market transactions have to be secured by collateral, a shortage of available collateral disrupts this intermediation. In this case, the connection between the central bank and non-banks is cut, and the liquidity provided by the central bank never reaches the non-bank financial sector. As a consequence, traditional policy tools have a limited effect on asset prices. Although the central bank can fully suppress the liquidity risk of traditional banks, it cannot prevent liquidity risk from growing in the non-bank sector. If this sector is large, asset prices remain substantially depressed regardless of any significant increase in central bank money made available to banks through liquidity operations.

In the last part of the analysis, we find that a central bank can further act on a liquidity crisis by directly purchasing large quantities of illiquid assets. By doing so, the central bank also removes the liquidity risk associated with the purchased assets from the economy, prevents asset prices from falling far below fundamental value and avoids a larger recession. The key element behind this positive effect is that the central bank itself never faces any liquidity risk, as its liabilities – central bank reserves – are considered money. Importantly, this channel can operate without a direct link between the central bank and non-banks. In other words, central bank asset purchases work through what economists refer to as a “general equilibrium” or “rising tide lifts all boats” effect and circumvent the bottleneck affecting liquidity from traditional central bank operations with banks.

Concluding remarks

Overall, our paper points to a potentially important fragility of the emerging financial structure: many institutions are performing liquidity transformation, thereby exposing them to liquidity risk, without the back-up of a central bank. In line with the US experience, our analysis indicates that opening emergency lending facilities to a broader set of institutions can be beneficial in reducing the fall of asset prices and, thereby, also limiting the magnitude of a financial crisis. In this regard, central bank swap agreements – under which central banks lend each other currencies – are crucial to provide liquidity to non-domestic institutions involved in foreign markets. Alternatively, an asset purchase programme from the central bank – commonly referred to as Quantitative Easing (QE) – may also play a key role in easing liquidity stress beyond the traditional banking sector. As the non-bank financial sectors grow, these new monetary policy tools are likely to be used again and become part of the usual toolkit of central banks, as currently demonstrated by the Fed’s responses to the coronavirus (COVID-19) crisis.

Having said this, our analysis is admittedly incomplete: while it stresses the potential benefits of providing liquidity to non-banks, it does not analyse the potential costs of doing so. After all, in exchange for their access to central bank liquidity, banks are regulated and continuously monitored. Central banks are thus in a good position to assess the quality of the collateral provided by banks, which may not be true of non-banks. Moreover, the expectation of access to central bank liquidity by non-regulated agents may generate moral hazard and thus lead to additional distortions. We leave these important topics for future research.

References

d’Avernas, A., Vandeweyer, Q., Darracq Pariès, M. (2020), “Unconventional Monetary Policy and Funding Liquidity Risk,” ECB Working Paper Series, No 2350.

Bernanke, B. (2009), “The Crisis and the Policy Response”, At the Stamp Lecture, London School of Economics, London, England.

European Systemic Risk Board (2019), “EU Non-bank Financial Intermediation Risk Monitor 2019”, Frankfurt-am-Main.

He, Z. and Krishnamurthy, A. (2013), “Intermediary Asset Pricing”, The American Economic Review, Vol. 103, No 2, pp. 732-770.

Mehrling, P. (2019), “The New Lombard Street: How the Fed Became the Dealer of Last Resort”, Princeton University Press, Princeton.

- Disclaimer: This article was written by Quentin Vandeweyer (Economist, Directorate General Research, Monetary Policy Research Division), Adrien d’Avernas (Assistant Professor, Stockholm School of Economics) and Matthieu Darracq Pariès (Deputy Head, Directorate General Economics, Forecasting and Policy Modelling Division). It is based on the ECB Working Paper no. 2350, “Unconventional Monetary Policy and Funding Liquidity Risk”, by the same authors. The authors gratefully acknowledge the comments of Michael Ehrmann, Alberto Martin, and Zoë Sprokel. The views expressed here are those of the authors and do not necessarily represent the views of the European Central Bank or the Eurosystem.