Liquidity distribution and settlement in TARGET2

Published as part of the ECB Economic Bulletin, Issue 5/2020.

1 Introduction

TARGET2, the payment system owned and operated by the Eurosystem, plays a vital role in the euro area, supporting the implementation of monetary policy as well as the functioning of financial markets and economic activity. Central banks and commercial banks use TARGET2 for monetary policy operations, interbank payments and customer payments.[2] The system processes euro-denominated payments in central bank money, on a gross basis, in real time and with immediate finality. It ensures the free flow of central bank money across the euro area, supporting economic activity, financial stability and promoting financial integration in the EU.[3] Moreover, TARGET2 has a global reach through correspondent banking,[4] which further supports the operations of EU banks and firms. Central bank liquidity – funds held by banks at the central bank, including the minimum reserves they must hold – is held on TARGET2 accounts and can be used to make payments throughout the day.

Liquidity plays a central role in real-time gross settlement (RTGS) systems, as without it no payment can be settled.[5] RTGS systems require considerable liquidity, as payments are settled one by one. They thus typically have features that enable participants to save liquidity. TARGET2 offers a number of such features to support participants in their intraday liquidity management.[6] In addition, participants can use the intraday credit line (ICL) facility offered by the Eurosystem when the liquidity on their accounts is not sufficient to settle payments.[7] They can also actively manage their payment flows, for example by synchronising their outgoing and incoming payments, thus making more efficient use of the liquidity available in the system. During periods of generally higher levels of liquidity, less effort is needed on the part of TARGET2 participants to manage their intraday liquidity and liquidity-saving mechanisms are used less.[8]

Liquidity availability and how liquidity is distributed have an impact on the settlement process. Although TARGET2 is operated as a single technical platform, it connects legally distinct component systems, each of which is operated by a national central bank. This article focuses on how liquidity is distributed across the various TARGET2 components and attempts to understand what this implies for payment settlement at jurisdiction level. In particular, it investigates how liquidity distribution across countries affects the reliance on intraday credit and the time of payment settlement. These aspects are important for the payment system operator:[9] a large intraday credit line increases the payment capacity[10] of the respective participant, making payment settlement smoother. Nevertheless, if a participant cannot repay its credit at the end of day, the latter is automatically transformed into overnight credit at the ECB’s marginal lending rate. The earlier payments are settled, the lower the operational risk.[11] Should an operational disruption occur during the day, the more payments have been settled up to that point, the lower the pressure on the system once it resumes settlement activity.

The remainder of the article is structured as follows. Section 2 provides an overview of liquidity distribution in TARGET2. Section 3 describes the implications of liquidity distribution for payment settlement in TARGET2. Section 4 concludes and discusses the relevance of the findings.

2 An overview of liquidity distribution in TARGET2

Liquidity in TARGET2 can be measured as the sum of the liquidity held by participants on their accounts at the beginning of each day.[12] Liquidity in TARGET2 increased by approximately eight times between mid-2008 and end-2019 (see Chart 1). It rose at the time of the sovereign debt crisis in 2011-12, amid measures taken by the Eurosystem to accommodate banks’ liquidity demand, and reached €592.7 billion in August 2012, compared with €219.8 billion in June 2008. The launch of the public sector purchase programme (PSPP) in March 2015 brought a new surge in liquidity levels. A peak of €1,847.2 billion was reached in August 2018. These developments resemble the evolution of excess liquidity, i.e. the funds held by credit institutions on accounts with the central bank in excess of minimum reserves.[13] With the increase in liquidity levels in TARGET2 following the start of the PSPP, the volatility of liquidity holdings at country level has decreased. Since end-2016 the country shares have broadly stabilised, with the exception of the Netherlands, whose share has decreased.[14]

Chart 1

Total liquidity in TARGET2 and liquidity by country

(left-hand scale: percentages of total liquidity; right-hand scale: total liquidity, EUR billions)

Sources: TARGET2 and ECB calculations.

Note: The data points represent monthly averages of daily data. Data cover the period from June 2008 to December 2019.

Most of the liquidity in TARGET2 is held by eight jurisdictions. Germany, France, the Netherlands, Italy, Spain, Finland, Belgium and Luxembourg account on average for 92.5% of the total liquidity held in TARGET2 (see Chart 1), broadly in line with the distribution of excess liquidity. Between June 2008 and December 2019 the share of liquidity held by Germany stood at an average of 28.2%, compared with 21.9% for France and 16.3% for the Netherlands. Italy held an average of 7.1%, Spain 6.2%, Finland 5.4%, Belgium 4.0% and Luxemburg 3.3%. The correlation between the liquidity available at country level and the value of TARGET2 payments is 0.92 over the same period. This suggests that jurisdictions with higher liquidity levels are also those which have higher payment activity in TARGET2. Germany, France and the Netherlands were the largest contributors to the TARGET2 traffic in 2019, in line with their liquidity share, accounting for around 68.0% of the value settled.[15] Luxembourg, Belgium, Spain and Italy followed, with shares ranging between 4.0% and 9.0%. The concentration of payment activity in a few countries is the consequence of a number of factors, including the size of the national banking system, the presence of financial market infrastructures, the location of banking groups’ headquarters and the role of institutions based in the country in providing access to TARGET2 to non-euro area banks.

Liquidity in TARGET2 is concentrated among a subset of institutions. Liquidity concentration is measured using the Gini coefficient,[16] which lies between zero (perfect equality) and one (maximum inequality). The Gini coefficient has ranged between 0.86 and 0.92 over time (see Table 1), indicating that most liquidity in TARGET2 is held by a few participants. This is broadly in line with the Gini coefficient calculated for minimum reserve requirements, which averaged 0.87 between the seventh reserve maintenance period in 2012 and the eighth maintenance period in 2019.[17] Thus the concentration of liquidity in TARGET2 largely reflects the concentration of banks’ minimum reserves and ultimately, as minimum reserve requirements are calculated on the basis of the banks’ balance sheets, market composition. The Gini coefficient for liquidity concentration increased first during the sovereign debt crisis in 2011-12, in line with the market fragmentation phenomenon observed at the time.[18] It also increased following the start of the PSPP. This suggests that the additional liquidity injected into the system ended up with participants that already had more liquidity on their accounts than others. On the other hand, the introduction of the two-tier system for the remuneration of excess reserves on 30 October 2019 led to a decrease in the concentration of liquidity holdings. Box 1 below discusses the impact of the introduction of the two-tier system on liquidity distribution in TARGET2 in greater detail.

The concentration of liquidity within euro area countries varies. Average figures for four periods between June 2008 and December 2019 show that concentration has ranged from 0.47 to 0.93 across all jurisdictions (see Table 1). The lowest concentration levels were recorded before the sovereign debt crisis, whereas the highest have been observed most recently. This is valid across jurisdictions, with very few exceptions. Since the start of the PSPP, Germany, Spain, France and the Netherlands have displayed the highest average concentration values, whereas Slovenia, Ireland and Malta have recorded the lowest. There is no clear impact of the PSPP on the concentration of liquidity at country level.

Table 1

Gini coefficient across euro area countries

Sources: TARGET2 and ECB calculations.

Note: Figures are not included for Malta before March 2015 and for Germany before September 2013 owing to data limitations.

Box 1 The impact of the two-tier system for remunerating excess liquidity on the distribution of liquidity in TARGET2

On 30 October 2019 the ECB introduced a two-tier system for remunerating excess liquidity holdings, which coincided with a redistribution of liquidity among the country components in TARGET2. Under the two-tier system, banks’ excess liquidity holdings are remunerated at 0% up to a limit of currently six times their minimum reserve requirements, creating an incentive for them to exploit any unused exemption allowances; excess liquidity above this level is subject to the rate on the deposit facility (currently -0.50%). Banks with excess liquidity holdings above the exemption allowances have an incentive to lend at negative rates more favourable to them than the deposit facility rate, while banks with unused exemption allowances can borrow funds at a negative rate and deposit them at 0% as part of the exempted tier. The exemption allowances can be filled on a domestic or cross-border basis. If the allowances are filled on a cross-border basis, liquidity is redistributed among the country components in TARGET2. In fact, according to ECB staff estimations based on excess liquidity data available prior to the introduction of the two-tier system, around 4% of exemption allowances, or around €30 billion, could only be filled if banks traded across borders.[19]

On 31 October, one day after the introduction of the two-tier system, Germany’s start-of-day balance registered a noticeable decrease, from €472.6 billion to €449.6 billion, as did that of Belgium, from €78.3 billion to €63.9 billion.[20] On the other hand, liquidity holdings of Italian banks in TARGET2 increased by €39.9 billion to €137.2 billion. In Spain, the TARGET2 start-of-day balance was not significantly altered the day after the introduction of the two-tier system, but in the course of five business days had changed by €13.0 billion. The new levels persisted until the end of the year. These moves in TARGET2 mirrored shifts in excess liquidity from liquidity-flush countries such as Belgium and Germany towards countries with unused allowances such as Italy (see Chart A). The redistribution of liquidity occurred mainly via secured transactions.

Chart A

TARGET2 start-of-day balances in selected jurisdictions around the introduction of the two-tier excess liquidity remuneration system

(EUR billions, daily data)

Sources: TARGET2 and ECB calculations.

Notes: Data cover the period from 2 September 2019 to 30 December 2019.

By 11 December 2019 banks had reduced their unused exemption allowances to 5%, from 28% on 30 October 2019,[21] which also resulted in a reduced concentration of liquidity in TARGET2. In particular, the Gini coefficient declined in Germany from 0.92 on average in the two months preceding the introduction of the two-tier system to 0.89 in the following two months. In Belgium the coefficient fell from 0.89 to 0.86, in Italy from 0.85 to 0.82 and in Spain from 0.88 to 0.86. These changes are significant, being equivalent to between two and seven times one standard deviation of the month-on-month changes since March 2015. Other jurisdictions that registered a decrease were Luxembourg, the Netherlands and Slovakia. Across all TARGET2 participants, liquidity concentration decreased from 0.90 to 0.89.

3 The impact of liquidity distribution on payment settlement in TARGET2

This section explores the link between liquidity distribution in TARGET2 and both the usage of credit lines and the time of payment settlement. Credit line usage and the time of payment settlement are both important factors in a smooth settlement process.

3.1 Usage of the intraday credit line

The ICL is a facility provided to TARGET2 participants by the Eurosystem, against eligible collateral.[22] The size of the credit line, which is interest-free, depends on the amount of collateral posted, which participants have the option to modify throughout the day. The ICL is automatically used by the system for payment settlement when liquidity on a participant’s TARGET2 account is insufficient. To ensure a smooth and timely settlement of payments, it is important for a participant to have a sizeable credit line. Nevertheless, if the credit is not repaid at the end of day, this amount automatically becomes subject to interest at the rate on the marginal lending facility. Thus an excessive reliance on intraday credit could expose participants to the risk of additional costs if they cannot repay the credit by the end of the day.

The total ICL has decreased in the context of the abundant levels of liquidity observed since March 2015. After the launch of the PSPP, the overall ICL decreased from €2,999.4 billion on average in March 2015 to €1,734.76 billion in December 2019. In the context of the PSPP and the asset purchase programme (APP) in general, the opportunity cost of holding collateral blocked for the ICL is higher than otherwise. This can at least partially explain the decline in the ICL. Prior to March 2015 the ICL constituted between 78.2% and 95.4% of participants’ overall payment capacity. With the recent abundant levels of liquidity, the payment capacity has been split almost evenly between the two sources. In December 2019, the ICL accounted for 49.4% of the payment capacity.

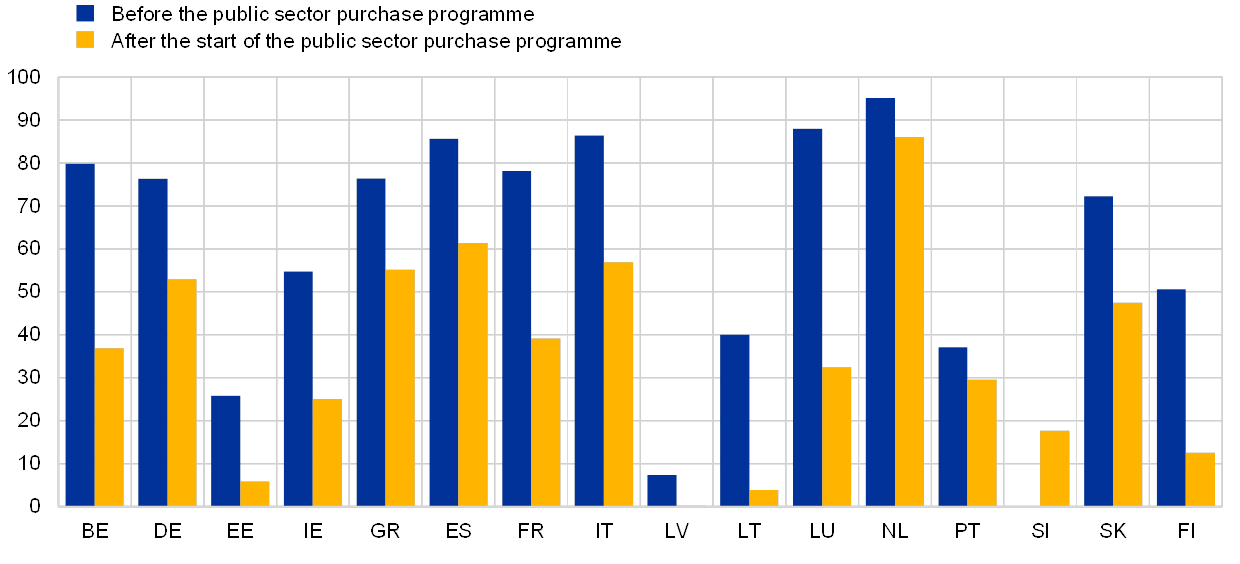

In jurisdictions which are large financial centres, the ICL makes up a large proportion of the payment capacity. Germany and France are the locations of large custodian banks, while Germany and the Netherlands have historically been used by non-euro area banks to access TARGET2. The ICL accounts for above 75% of the payment capacity in these jurisdictions (see Chart 2). These are also the jurisdictions that hold the largest ICLs in absolute value and the largest holders of liquidity in TARGET2. In terms of ICL usage, i.e. the share of the ICL that is actually used to make payments,[23] however, they stand in the middle range, with values between 20.0% and 34.0% (see Chart 3). Overall, these figures suggest that the large ICL values are a consequence of the role that these jurisdictions play as financial centres, which results in large holdings of collateral. Assuming that any collateral that is not used otherwise (e.g. for open market operations) is allocated to ICLs, ICLs will be large. Large ICLs cannot therefore be interpreted as demand-driven. Other jurisdictions, such as Belgium, Greece, Spain, Italy or Luxembourg, also have payment capacity composed mainly of ICLs, but with ICLs in absolute terms much lower than in Germany, France or the Netherlands.

Chart 2

Intraday credit lines in TARGET2 relative to total payment capacity by jurisdiction

(percentages of total payment capacity per jurisdiction)

Sources: TARGET2 and ECB calculations.

Note: Data cover the period from June 2008 to December 2019. The chart shows euro area countries only. Owing to data limitations, the calculation does not include figures for Austria, Malta, Germany before September 2013, Latvia before January 2014, Portugal before April 2009 and Slovenia before November 2015.

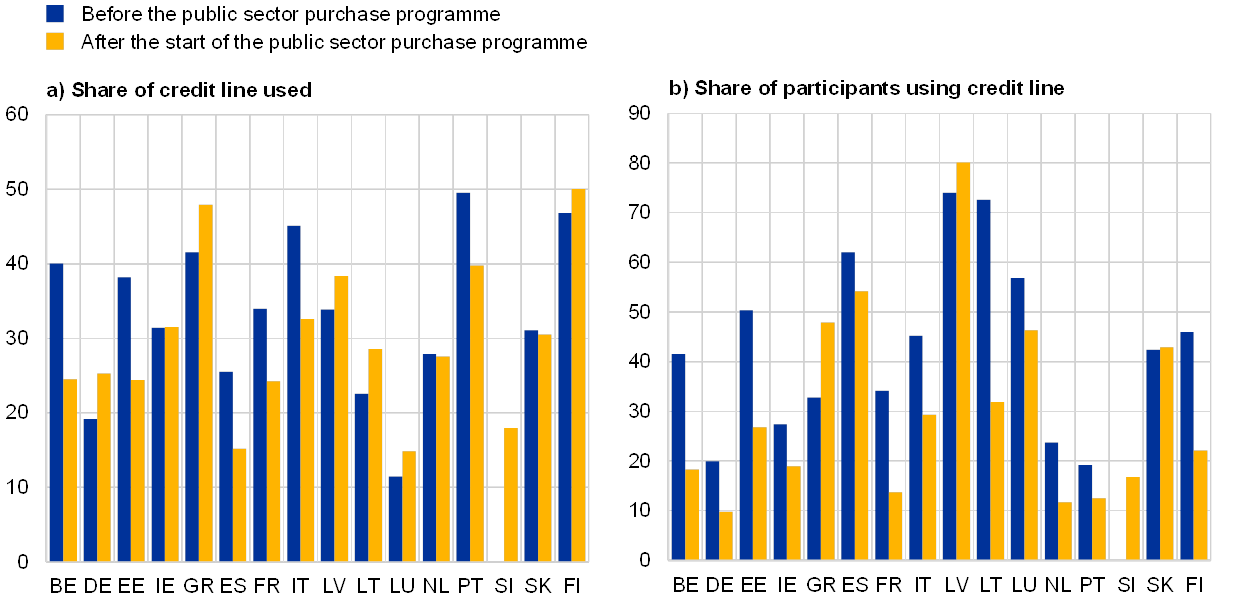

Given relatively limited ICL usage, a large component of the ICL seems to be supply-driven. ICL usage stands at around 31.4% on average across jurisdictions and different time periods, fluctuating between 11.5% and 50.0% (see Chart 3). Among the jurisdictions with the highest use of ICL are Greece, Italy, Portugal and Finland. The jurisdictions with the lowest use are Germany, Spain and Luxembourg. The variation in ICL usage may depend on whether the ICL is more supply or demand-driven, as well as on how well banks manage their liquidity on an intraday basis. The number of participants that actually use the ICL is also limited. In the context of abundant levels of liquidity, only approximately 10.4% of the participants in TARGET2 use the ICL, down from 31.9% in March 2015. This generally holds true across jurisdictions, which constitutes an additional indication that a large component of the ICL is actually supply-driven. Moreover, the collateral posted for the ICL can do a “double duty”, i.e. also count as collateral that banks have to hold for prudential purposes (e.g. liquidity buffers and high-quality liquid assets to be maintained under the liquidity coverage ratio rules). When the size of the ICL coincides with the collateral that banks have to hold for prudential purposes, the opportunity cost of having it blocked for the ICL becomes zero, and having access to a large ICL makes it easier for banks to manage intraday liquidity as it augments their payment capacity.

Chart 3

Usage of the intraday credit line across jurisdictions

(percentages)

Sources: TARGET2 and ECB calculations.

Note: Data cover the period from June 2008 to December 2019. The chart shows euro area countries only. Owing to data limitations, the calculation does not include figures for Austria, Malta, Germany before September 2013, Latvia before January 2014, Portugal before April 2009 and Slovenia before November 2015.

To understand better how liquidity availability at jurisdiction level relates to the use of the ICL, a panel study is conducted. This approach allows the value of payments settled, the size of the credit line, the concentration of liquidity, and the intraday coordination of payments to be simultaneously taken into account. Given the same level of liquidity, jurisdictions that settle more payments should also use the ICL more. Use of the ICL could also be higher if the same liquidity level is available but liquidity is concentrated in the hands of fewer participants. The intraday coordination of payments is also relevant for the use of the ICL. By synchronising payments, it is possible to use liquidity more efficiently, and recourse to the ICL should be thus more limited. In addition, the overnight interest rate, which gives the cost of liquidity, is added as a control. An increase in the cost of liquidity is an incentive for participants to make greater use of intraday credit, which bears no interest.

Results show that jurisdictions that hold more liquidity use the ICL less. The results are statistically significant across specifications (see Table 2). According to the most comprehensive specification (specification (3) in Table 2), a €63 billion increase in liquidity (start-of-day liquidity) – equivalent to one standard deviation of liquidity holdings across countries averaged over time – corresponds to a decrease of 1.3 percentage points in the use of the ICL. The size of the ICL is also negatively correlated with its use. This result supports the observation made previously that the size of the ICL seems to have a strong supply component, i.e. the jurisdictions that hold a large credit line need it less. Regarding the concentration of liquidity (Gini coefficient), the coefficients are not statistically significant, while the negative relationship holds across all specifications. Finally, a 1 percentage point increase in the cost of liquidity (the overnight unsecured rate) corresponds to a 2.5 percentage point increase in the use of the ICL.

Jurisdictions that are better at coordinating their payments use the ICL less. Payment coordination is measured as the time spread that each jurisdiction needs on average to settle the core 40%-60% of their payments.[24] This means that as the time spread increases, coordination decreases. As expected, jurisdictions in which participants better synchronise their incoming payments with outgoing payments manage to economise on usage of the liquidity available on their TARGET2 accounts and are less in need of the ICL (see specifications (2) and (3) in Table 2). An improvement in the coordination of payments by 66 minutes – representing one standard deviation in the coordination measure across jurisdictions and averaged across time – is reflected in a decrease of 1.1 percentage points in the use of the ICL.

Table 2

Panel analysis on the usage of the intraday credit line

Sources: ECB, TARGET2 and ECB calculations.

Notes: Data cover the period from June 2008 to December 2019. The overnight unsecured rate is measured as the EONIA until 1 October 2019 and the €STR from then onwards. The reported results are based on fixed effects regressions. Robust standard errors are reported in parentheses. *** p<0.01, ** p<0.05,* p<0.1. Owing to data limitations, the calculation does not include figures for Austria, Malta, Germany before September 2013, Latvia before January 2014, Portugal before April 2009 and Slovenia before November 2015.

3.2 Time of payment settlement

The time of payment settlement depends on liquidity availability. In general, payments are settled soon after they enter the system,[25] provided that participants have sufficient payment capacity. Higher payment capacity can thus lead to earlier settlement, whereas a constraint in the payment capacity, such as during times of stress, might lead to later settlement. The degree of concentration of liquidity might also affect payment processing if there is a significant discrepancy between the participants holding most of the liquidity and those sending most payments. Another important factor determining the time of payment settlement is active management of payment flows on the part of TARGET2 participants, which can support earlier settlement by synchronising incoming and outgoing payments.[26] The timing of payment settlement is very important from an operational point of view: the earlier payments are settled, the lower the operational risk. Should an operational disruption occur during the day, the more payments have been settled up to that point, the lower the pressure on the system once it resumes settlement activity.

The time of payment settlement in TARGET2 has responded to changes in liquidity levels over the years. The average time of payment settlement moved during the sovereign debt crisis to 12:34 CET, from 12:08 CET in June 2008.[27] In 26 minutes during the sovereign debt crisis – equivalent to the difference between the two average times of settlement –TARGET2 settled payments worth approximately €84.5 billion[28]. Also at that time liquidity concentration increased, suggesting that fragmentation may have made it more difficult for some jurisdictions to fund their payments, owing either to limited liquidity availability or to the reluctance of counterparties to send payments to participants that were in need of liquidity. When liquidity is limited, payments can spend a longer time in the queue waiting to be settled. Since the start of the PSPP and with the consequent increase in liquidity, the average time of payment settlement has become earlier, from 12:25 CET in March 2015 to 11:46 CET in December 2019. In 2019 TARGET2 settled payments worth on average €93.0 billion[29] in a 39-minute interval. These changes are also reflected in the intraday pattern of payment settlement (see Chart 4). The impact of the financial and sovereign debt crises is more visible in the settlement of payments from the fourth up to the eighth decile. At the beginning of the day TARGET2 processes a large number of customer payments, whereas interbank activity intensifies later in the day.[30] As interbank activity is typically more severely affected in situations of financial turmoil, it is reasonable to expect a smaller impact on the first payment deciles. Another downward move in the timing of the same set of payments can be observed just after the PSPP started, as well as towards the end of 2018 until the first half of 2019. The launch of TARGET2-Securities (T2S) in mid-2015, and the consequent migration of central securities depositories (CSDs),[31] could have also had an impact on the average time of payment settlement, as it resulted in a shift of traffic from TARGET2 to T2S. Nevertheless, this impact cannot be disentangled from the impact of the PSPP, as the time periods largely overlap.

Chart 4

Times of settlement by payment value deciles

(time of settlement)

Sources: TARGET2 data and ECB calculations.

Note: Data cover the period from June 2008 to December 2019. Technical transactions and liquidity transfers are not included in the calculations.

The average time of payment settlement varies significantly from country to country. The average time of payment settlement varies between 08:00 CET and 13:17 CET across countries (see Chart 5). A simple comparison of the average times by country does not appear to suggest a clear link between liquidity holdings and times of payment settlement. After the start of the PSPP, payments were settled earlier on average in most jurisdictions. The changes ranged from around 30 seconds in the case of Austria to almost 2.5 hours for Ireland. At the same time, Greece, Germany and Luxembourg experienced slightly later average times of payment settlement, albeit by less than 15 minutes.

Chart 5

Average time of payment settlement by jurisdiction

(time of settlement)

Sources: TARGET2 and ECB calculations.

Note: Data cover the period from June 2008 to December 2019. The average settlement time is calculated as a value-weighted average. Technical transactions and liquidity transfers are not included in the calculations.

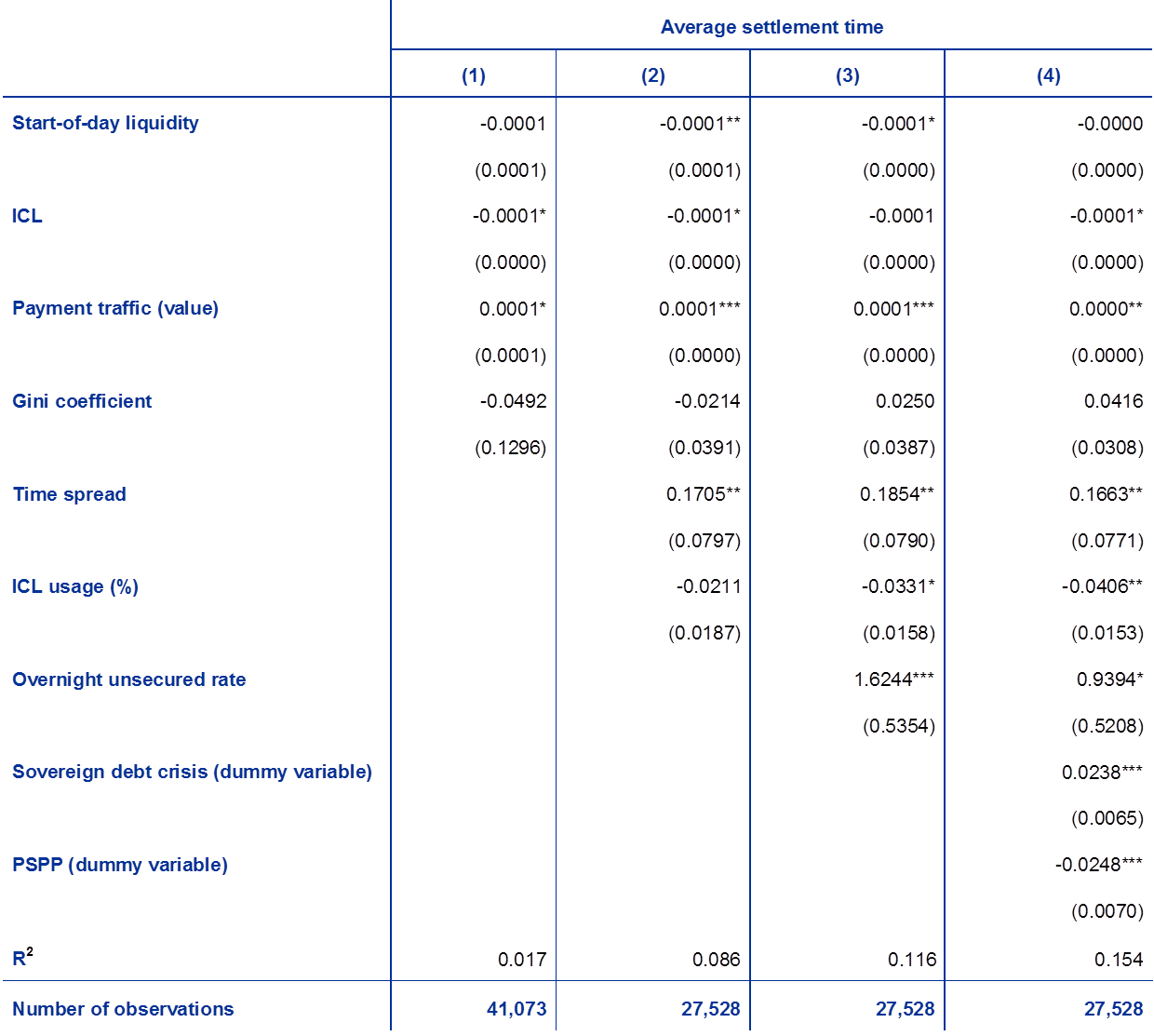

Countries with larger payment capacity display on average earlier times of payment settlement. This result emerges from a panel analysis in which the start-of-day balances and ICL (both set and used), TARGET2 traffic, liquidity concentration and the intraday coordination of payments are controlled for (see Table 3). In addition, time dummies are introduced for the period of the sovereign debt crisis in 2011-12 and for the start of the PSPP in March 2015. Both start-of-day liquidity and the ICL set are negatively correlated with the average time of payment settlement and the coefficients are in the same range. In other words, greater payment capacity is associated with earlier times of payment settlement. On average, a €63 billion increase in liquidity – equivalent to one standard deviation of liquidity holdings across countries averaged over time – corresponds to a decrease of approximately four minutes in the average time of payment settlement. However, the relationships are not consistently significant across specifications. Greater recourse to the ICL (ICL usage) is also associated with earlier average times of payment settlement, showing that, when participants are willing to tap into their credit lines, it is beneficial for the settlement process.

Jurisdictions with greater payment coordination tend to experience earlier times of payment settlement. Across all specifications, when payments are more dispersed over the day (in other words, less synchronised), the average time of payment settlement is later (see specifications (2), (3) and (4) in Table 3). A 66 minute decrease in the dispersion of payments results in the average time of payment settlement being approximately 11 minutes earlier. Likewise, the higher the TARGET2 traffic, the later the average time of settlement. This seems reasonable: given the same level of liquidity, more payments should take longer to be processed. The coefficient of liquidity concentration (Gini coefficient) is not statistically significant for any specification. As mentioned above, liquidity concentration might influence the time of settlement if there is a significant discrepancy between the participants holding most of the liquidity and those sending most payments. This result suggests that in TARGET2 liquidity concentration is in line with payment concentration. Finally, higher overnight unsecured rates, which measure the cost of liquidity, lead to later average times of payment settlement.

Table 3

Panel analysis on the average payment settlement time

Sources: ECB, TARGET2 and ECB calculations.

Notes: Data cover the period from June 2008 to December 2019. The overnight unsecured rate is measured as the EONIA until 1 October 2019 and the €STR from then onwards. The reported results are based on fixed effects regressions. Robust standard errors are reported in parentheses. *** p<0.01, ** p<0.05,* p<0.1. Owing to data limitations, the calculation does not include figures for Austria, Malta, Germany before September 2013, Latvia before January 2014, Portugal before April 2009 and Slovenia before November 2015.

4 Conclusion

Liquidity is essential in the settlement process. This article has taken stock of how major aspects of payment settlement have changed under different liquidity regimes. In line with developments in excess liquidity, the amount of liquidity in TARGET2 increased by approximately eight times between 2008 and 2019, as a direct consequence of the monetary policy measures taken. While liquidity levels varied throughout this period, the most visible changes emerged in the context of the abundant levels of liquidity resulting from the extensive asset purchase programme carried out by the Eurosystem. The average time of payment settlement was brought down from 12:25 CET to 11:46 CET, which has contributed to a reduction in operational risk. The payment capacity is now more balanced, being almost equally split between the liquidity available on TARGET2 accounts and intraday credit. The ICL is used less to settle payments and fewer participants make use of it. An excessive use of the ICL can lead to the use of the marginal lending facility at the end of the day, which incurs a cost for the participant. While these aspects are beneficial for the smooth settlement of payments, they should not be interpreted as essential. Historical developments show that TARGET2 was able to settle even larger payment values than it currently does with less liquidity available in the system.

These observations, which hold for TARGET2 as a whole, are also true for the system’s components, although heterogeneity exists. 66.4% of the liquidity in TARGET2 is held by three jurisdictions, namely Germany, France and the Netherlands. These have very high ICLs, and ICLs account for a large part of their payment capacity, although usage is limited. The size of the credit line in these jurisdictions seems to be significantly supply-driven. Figures for other jurisdictions are less conclusive in this respect. As an overview across different periods and jurisdictions, the ICL has represented between 0.0% and 95.2% of the payment capacity, usage of the ICL has varied between 11.5% and 50.0%, and the share of participants using the credit line has been between 9.8% and 80.2%. The average time of payment settlement has varied between 08:00 CET and 13:17 CET, while concentration of liquidity has also differed across countries, ranging on average between 0.47 and 0.93. Liquidity concentration in TARGET2 is nevertheless broadly in line with the concentration of minimum reserves, indicating that it is largely a consequence of market composition.

Across jurisdictions, larger holdings of liquidity are associated with a lower use of the ICL and an earlier time of settlement. This conclusion emerges from the panel analysis conducted. A €63 billion increase in liquidity – equivalent to one standard deviation of liquidity holdings across countries averaged over time – corresponds to a decrease of 1.3 percentage points in the use of the ICL and an average time of payment settlement four minutes earlier. At the same time, an improvement in the coordination of payments by 66 minutes – representing one standard deviation in the coordination measure across jurisdictions and averaged across time – is reflected in a decrease of 1.1 percentage points in the use of the ICL and an average time of payment settlement 11 minutes earlier. The changes are comparable in size, suggesting that improvements beneficial for the settlement process can be achieved equally by increasing liquidity or making a greater effort to synchronise payments.

- The authors of this article are members/alternates of one of the user groups with access to TARGET2 data in accordance with Article 1(2) of Decision ECB/2010/9 of 29 July 2010 on access to and use of certain TARGET2 data. The ECB, the Market Infrastructure Board and the Market Infrastructure and Payments Committee have checked the article against the rules for guaranteeing the confidentiality of transaction-level data imposed by the Payment and Settlement Systems Committee pursuant to Article 1(4) of the abovementioned ECB Decision. The views expressed in the article are solely those of the authors and do not necessarily represent the views of the Eurosystem. The authors thank Carlos Luis Navarro Ramirez for research assistance.

- For instance, if an airline company in the Netherlands acquires an aeroplane from a company in France, the transfer of the payment can be made in TARGET2 via their banks. Other payment and securities settlement systems such as EURO1, a pan-European large-value payment system, and STEP2, a pan-European retail payment system, also settle their participants’ net positions in TARGET2.

- In 2019 TARGET2 settled an average of €1.7 trillion on a daily basis, corresponding to 344,120 transactions (see TARGET Annual Report 2019, ECB, Frankfurt am Main, May 2020).

- A correspondent bank is a bank that provides services on behalf of another bank.

- When a payment message is sent to the system, the payment is settled immediately if the participant has enough liquidity on its account. As soon as the sender’s account has been debited, the payment becomes irrevocable. If liquidity on the sender’s account is not sufficient to settle the payment, the payment is placed in a queue.

- For instance, offsetting algorithms, which match and offset payments at entry or while they are in the queue.

- The ICL is offered, free of interest, against eligible collateral that participants post with their national central banks. At the end of the day, if the participant cannot cover its negative position, the intraday credit becomes overnight credit charged at the rate on the marginal lending facility.

- For example, in mid-2014 a daily average of €2.0 trillion worth of payments were settled in TARGET2, against an overall liquidity level of €200.7 billion. In mid-2019, approximately €1.8 trillion in payments were settled each day, but liquidity levels stood at €1,790.5 billion as a consequence of monetary policy measures under the asset purchase programme, i.e. fewer payments were settled with higher liquidity. The difference lies in how efficiently liquidity is used: in mid-2014 an indicator showing the efficiency of the liquidity used in TARGET2 stood at 5.0, while in mid-2019 it stood at 3.3. The efficiency of the liquidity used is computed as the ratio of total payments settled to an estimated level of liquidity used, following Benos, E., Garratt, R. and Zimmerman, P., “Bank behaviour and risks in CHAPS following the collapse of Lehman Brothers”, Working Paper Series, No 451, Bank of England, June 2012.

- Payment systems may be owned and operated by a central bank or by the private sector. In its role as owner and operator of TARGET2, the Eurosystem offers settlement in central bank money by allowing financial institutions to transfer funds held in accounts with their central bank to each other. Acting in an operational capacity is one way for a central bank to ensure that the system meets the safety and efficiency standards it has set.

- The payment capacity of a TARGET2 participant at the start of the business day is defined as the sum of the opening balance on its account and the amount of the ICL set.

- See e.g. McAndrews, J. and Kroeger, A., “The Payment System Benefits of High Reserve Balances”, Staff Reports, No 779, Federal Reserve Bank of New York, June 2016.

- Start-of-day balances are adjusted for the use made overnight of the Eurosystem’s standing facilities (the marginal lending facility and the deposit facility). Further adjustments are applied to correct for national specificities. In particular, some central banks use proprietary home accounts, to which their participants’ liquidity is moved at the end of the day. This is done, for instance, for the computation of the minimum reserves credit institutions are required to hold with their central bank, as the Reserve Management Module in TARGET2 is optional.

- See Baldo, L., Hallinger, B., Helmus, C., Herrala, N., Martins, D., Mohing, F., Petroulakis, F., Resinek, M., Vergote, O., Usciati, B. and Wang, Y., “The distribution of excess liquidity in the euro area”, Occasional Paper Series, No 200, ECB, Frankfurt am Main, November 2017.

- The developments observed in the latter part of 2019 can be explained by the fact that some credit institutions based in the United Kingdom have relocated their point of access to TARGET2 from the Netherlands to France and Germany in view of Brexit.

- See TARGET Annual Report 2019, ECB, Frankfurt am Main, May 2020.

- The Gini coefficient has been adopted in payment system-related literature to measure inequality from different perspectives. Another measure of concentration widely used is the Herfindahl-Hirschman Index (HHI). See e.g. Adams, M., Galbiati, M. and Giansante S., “Liquidity costs and tiering in large-value payment systems”, Working Paper Series, No 399, Bank of England, July 2010; Denbee, E., Garratt, R.J. and Zimmerman, P., “Variations in liquidity provision in real-time payment systems”, Working Paper Series, No 513, October 2014, revised January 2015; McAndrews, J. and Kroeger, A., “The Payment System Benefits of High Reserve Balances”, Staff Reports, No 779, Federal Reserve Bank of New York, New York, June 2016.

- The ECB started collecting individual minimum reserve requirement data from national central banks as of the seventh reserve maintenance period of 2012.

- Eisenschmidt, J., Kedan, D., Schmitz, M., Adalid, R. and Papsdorf, P., “The Eurosystem’s asset purchase programme and TARGET balances”, Occasional Paper Series, No 196, ECB, Frankfurt am Main, September 2017.

- See A tale of two money markets: fragmentation or concentration, speech by Benoît Cœuré at the ECB workshop on money markets, monetary policy implementation and central bank balance sheets, Frankfurt am Main,12 November 2019.

- Since start-of-day balances are used to measure liquidity in TARGET2, the changes are visible only one day after.

- See the box entitled “Market reaction to the two-tier system”, Economic Bulletin, Issue 8, ECB, 2019.

- See Guideline (EU) 2015/510 of the European Central Bank of 19 December 2014 on the implementation of the Eurosystem monetary policy framework (ECB/2014/60) (OJ L 91, 2.4.2015, p. 3).

- The ICL usage is calculated as the ratio of the maximum credit used from the intraday credit line throughout the day relative to the credit line set.

- Payment coordination is measured as: , where represents the average time by which of the payments are settled. The measure was developed for a forthcoming paper on wholesale payment system liquidity by the Committee on Payments and Market Infrastructures (Bank for International Settlements) Expert Group on RTGS Liquidity Efficiency.

- In TARGET2, payments are typically processed in less than five minutes (see TARGET Annual Report 2019, ECB, Frankfurt am Main, May 2020). In other words, less than five minutes pass between the time at which the payment enters the system – the “introduction time” – and the time at which the payment is settled – the “settlement time”.

- Aside from payments that need to be settled at particular times of the day, such as those related to the settlement of ancillary system positions, participants are free to manage their payment flows.

- TARGET2 operates during both the day, between 07:00 CET and 18:00 CET, and during the night, between 19:30 CET and 22:00 CET and between 01:00 CET and 07:00 CET. The average settlement time is calculated as a value-weighted average based on TARGET2 payments settled during the day.

- The figure is computed as a daily average based on traffic in the period 2011-12 and assumes that payments are evenly spread throughout the day. It should thus be interpreted with caution.

- The figure is computed as a daily average based on 2019 traffic and assumes that payments are evenly spread throughout the day. It should thus be interpreted with caution.

- See TARGET Annual Report 2019, ECB, Frankfurt am Main, May 2020.

- T2S allows the exchange of cash and securities via a single point, as the platform hosts 21 CSDs from 20 European markets. The migration of CSDs started in September 2015 and ended in September 2017.